7 Best Budget Apps for ADHD (+FREE)

I used to think budgeting was just… not for me.

I’d set up a fancy spreadsheet, track my expenses for a week, and then forget about it entirely.

ADHD and traditional budgeting? A total mismatch.

But then I realized I wasn’t the problem—the system was.

I needed tools designed for the way my brain actually works.

So, I went down a rabbit hole, testing every budgeting app I could get my hands on.

Some were a disaster, some were ‘meh,’ and a few?

Absolute game-changers.

Let’s talk about the best budgeting apps for ADHD that actually make sense.

Table of Contents

- 1. You Need A Budget (YNAB) – I Like it the Most

- 2. Snoop Money – Best Free Option

- 3. Weekly – Best for ADHD-Friendly Budgeting Approach

- 4. Monarch Money – Best for Financial Management

- 5. PocketGuard – Best for Preventing Overspending

- 6. Copilot – Best for Customizable Budgeting

- 7. Quicken Simplifi – Best for Simplified Budgeting

- My Final Take

- FAQs

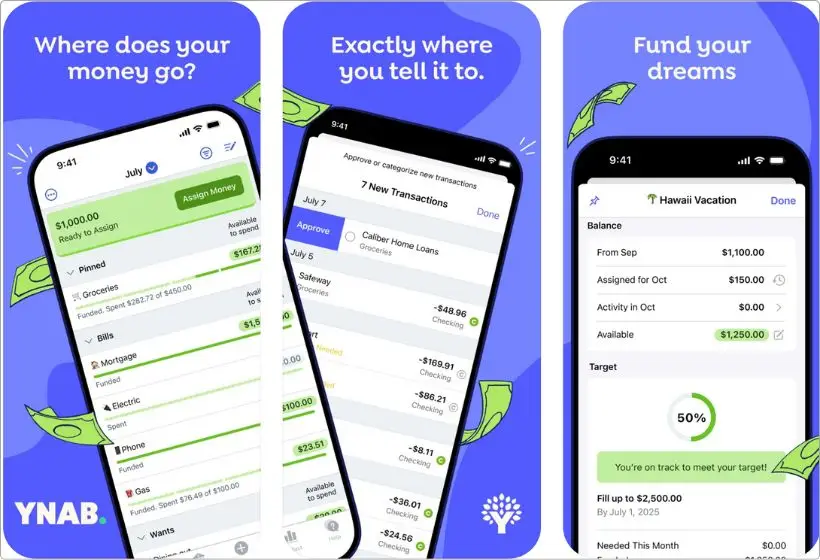

1. You Need A Budget (YNAB) – I Like it the Most

Pros:

- Uses zero-based budgeting to give every dollar a job.

- Helps ADHD users plan ahead and avoid impulsive spending.

- Syncs across devices in real-time, great for couples/families.

- Powerful automation and goal tracking.

Cons:

- Takes time to get used to.

- Requires manual input at times (bank sync isn’t perfect).

- Subscription-based.

Price: $14.99/month or $109/year.

Get it from: App Store

I’ll be honest—when I first tried You Need A Budget (YNAB), I hated it.

Yep, straight-up hated it.

It wasn’t just another budgeting app where I could dump my expenses and move on.

No.

YNAB actually forced me to pay attention to my money, which (let’s be real) was something I wasn’t used to doing.

But then, something weird happened.

I started getting better with my money.

Bills? Covered.

Savings? Growing.

Impulse spending? Finally under control.

And that’s when it clicked.

YNAB isn’t just an app, it’s a budgeting system.

It follows a zero-based budgeting method, meaning every dollar you earn has a job.

It’s like giving your money a purpose so you don’t accidentally blow it on stuff you don’t even remember buying.

What makes the YNAB app amazing for ADHD?

First, the real-time syncing is a lifesaver.

Whether you’re on your iPhone, iPad, or desktop, everything updates instantly.

No more forgetting if you already logged an expense (which, let’s be honest, happens a lot).

Then, there’s the goal-setting feature.

Instead of just tracking spending, YNAB helps you actively plan ahead—which is crucial when you struggle with financial impulse control.

Now, let’s talk about the learning curve.

Because, yeah, it exists.

YNAB isn’t an install-and-forget kind of app.

It takes time to get used to (you’ll probably be frustrated at first).

But once you push through that, you’ll see why YNAB users are borderline cult-like in their loyalty.

Is it worth paying for?

Absolutely.

If you’re serious about taking control of your money.

The $14.99/month or $109/year price tag stings at first, but YNAB easily saves you way more than that by stopping bad spending habits.

If you’re tired of feeling like your money is controlling you instead of the other way around, YNAB is worth a shot.

Also read: Best routine apps for ADHD

2. Snoop Money – Best Free Option

Pros:

- Free to use.

- AI-powered insights help ADHD users.

- Automatically finds savings on bills and subscriptions.

- Tracks multiple bank accounts in one place.

- Sends reminders for upcoming bills and payments.

Cons:

- UK-based—some features may not work outside the UK.

- Requires connecting bank accounts (some people might not be comfortable with that).

Price: Free, £3.99/month, or £39.99/year.

Get it from: App Store

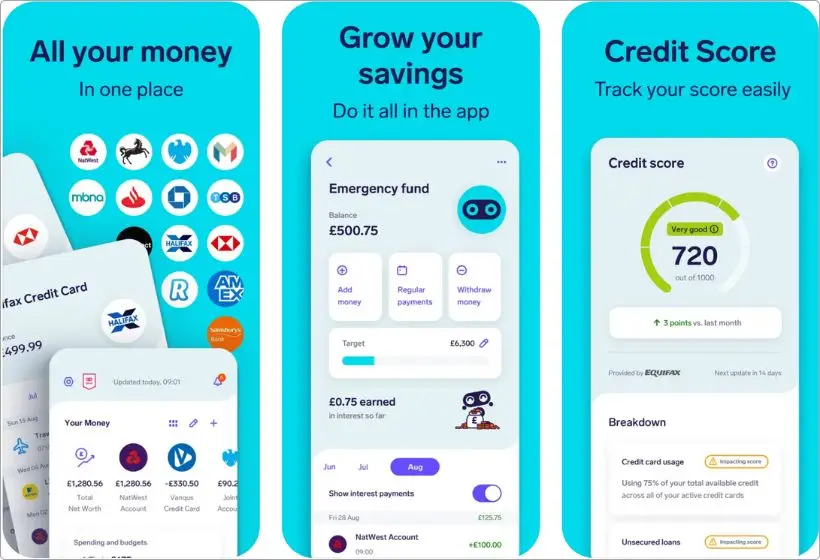

Alright, let’s talk about Snoop Money.

I’ll be real with you—before I started digging into budgeting apps, I had no idea this one even existed.

But wow, this app is a total game-changer, especially if you’re looking for a free budgeting tool that actually helps ADHD brains stay on track.

So, what makes Snoop special?

First off, it’s free to use.

While there are paid plans, the free version offers plenty for most users.

If you’d like a deep dive into the free vs. paid features, let me know in the comments.

That alone makes it a solid pick, especially if you’re just getting started with budgeting and don’t want to commit to a paid app like YNAB or Copilot.

But what really makes Snoop stand out is its AI-powered insights.

It doesn’t just track your spending—it actively analyzes your financial habits and gives you helpful nudges.

Another thing I love?

It finds ways to save you money.

Snoop constantly scans your bank transactions and lets you know if you’re overpaying on subscriptions, bills, or even groceries.

If there’s a better deal out there, it tells you.

Now, let’s talk about the downside.

Since Snoop is UK-based, some features (like automatic bill switching) might not work outside the UK.

But if you just need a FREE budgeting app for ADHD, Snoop is 100% worth checking out.

Also read: Best ADHD reminder apps

3. Weekly – Best for ADHD-Friendly Budgeting Approach

Pros:

- Uses a weekly budgeting system.

- Helps prevent overspending.

- Simple and visually clean interface.

Cons:

- No investment tracking.

- Subscription-based.

Price: $7.99/month or $47.99/year.

Get it from: App Store

I’ve always struggled with monthly budgeting.

No matter how hard I tried to track my expenses for 30 days, I’d lose track by Week 2 and end up spending way too much, too fast.

Then the rest of the month? Total chaos.

Sound familiar?

If so, you definitely need to try this Weekly app.

It’s built for people who need to think about money in shorter time frames.

Instead of giving you a big monthly budget (which is easy to mess up), it breaks your spending into weekly chunks, making it way easier to stay on track.

Here’s how it works: You set your income, subtract fixed expenses (like rent, bills, and savings), and whatever’s left is divided into weekly spending limits.

It’s like giving yourself a fresh start every seven days, and it’s perfect for ADHD brains that struggle with long-term planning.

Another thing I love? Simplicity.

This app isn’t trying to be YNAB or Monarch—it’s not packed with features, and that’s actually a good thing if you get overwhelmed by complex budgeting tools.

The interface is clean, easy to understand, and distraction-free.

But let’s be real, Weekly isn’t for everyone.

If you need investment tracking, you won’t find them here.

This app is laser-focused on day-to-day spending control.

Also, while it’s cheaper than YNAB ($7.99/month or $47.99/year), it’s still a paid app—so keep that in mind.

Bottom line?

If traditional budgeting overwhelms you and you just want something simple to stop overspending, Weekly is a fantastic choice.

Also read: Best ADHD Planner apps

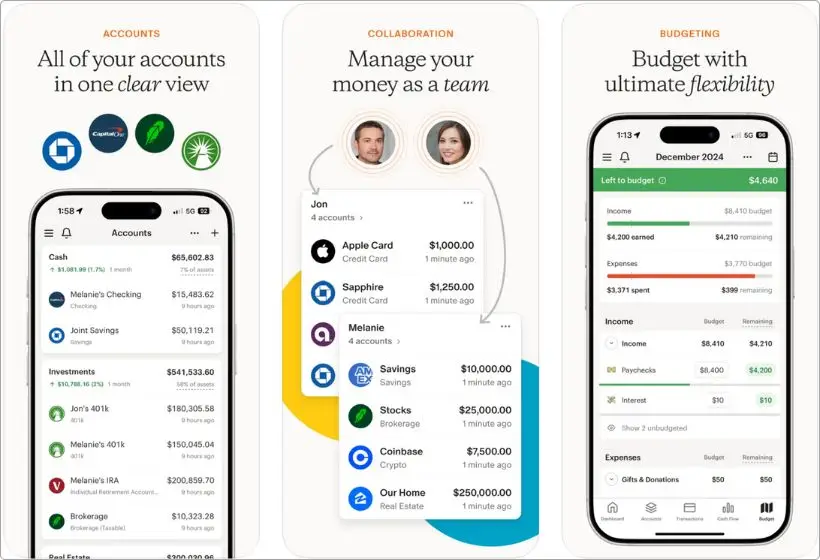

4. Monarch Money – Best for Financial Management

Pros:

- All-in-one financial dashboard.

- Bank syncing is fast and reliable.

- Goal-setting and collaborative budgeting.

- Web and mobile versions work seamlessly together.

Cons:

- No free version.

- Can feel overwhelming if you just need basic budgeting.

Price: $14.99/month or $99.99/year.

Get it from: App Store

I’ll be honest—some budgeting apps feel like they were built for accountants.

They’re packed with numbers, graphs, and so much data that my brain just shuts down.

That’s why Monarch Money caught my attention.

It takes all those complicated financial tools and makes them ADHD-friendly.

So what makes Monarch different?

First, it’s an all-in-one financial management tool.

Instead of juggling multiple apps for investing, saving, and budgeting, everything is in one place.

That means fewer distractions and less app-hopping, which is a win if you struggle with focus.

One of my favorite features is collaborative budgeting.

If you manage finances with a partner (or just want someone to keep you accountable), you can share your budget and goals in real-time.

The app also has strong bank syncing, which updates your transactions quickly (unlike some apps that take forever).

Plus, goal-setting features help ADHD users stay motivated.

Want to save for a trip, pay off debt, or build an emergency fund?

Monarch keeps you focused with clear progress tracking.

But it’s not free.

At $14.99/month or $99.99/year, it’s almost the same price range as YNAB.

Also, if you’re looking for just a basic budgeting tool, Monarch might feel like overkill.

However, if you want a full financial command center that keeps you on track without overwhelming you, Monarch Money is 100% worth it.

Also read: Best ADHD calendar apps for iPhone

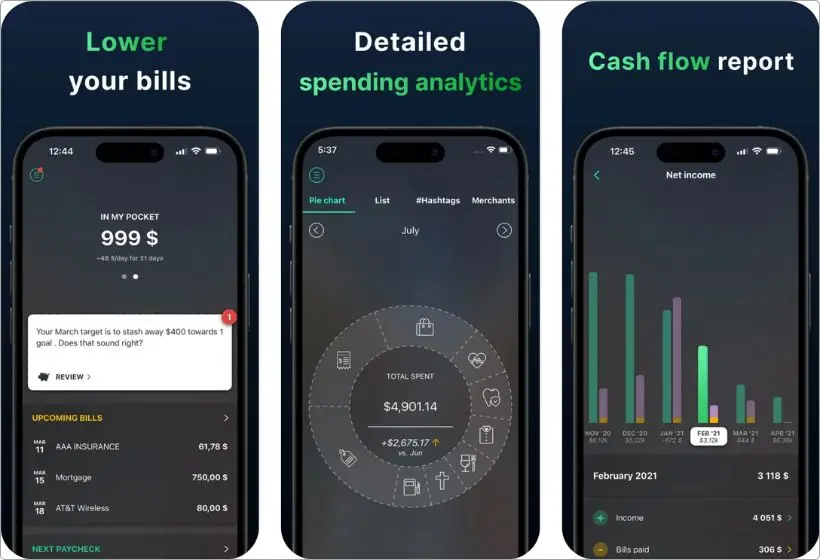

5. PocketGuard – Best for Preventing Overspending

Pros:

- “In My Pocket” feature shows exactly how much you can safely spend.

- Automatically tracks bills, income, and spending.

- Bank syncing is reliable and updates transactions quickly.

- Real-time spending insights.

Cons:

- Free version has limited features.

- No detailed investment tracking.

Price: $7.99/month or $74.99/year.

Get it from: App Store

Let’s be real—impulse spending is a HUGE struggle for ADHD brains.

You see something cool, get a dopamine rush, and before you know it, your bank account is crying.

If that sounds like you, PocketGuard might be your new best friend.

The best thing about PocketGuard?

It literally tells you how much you can safely spend.

Instead of making you dig through spreadsheets or guess if you can afford takeout tonight, its “In My Pocket” feature does the math for you.

It calculates your income, bills, savings goals, and upcoming expenses, then gives you a clear number of how much money is actually available.

For ADHD users, this kind of clarity is a game-changer.

There’s no need to overthink or second-guess your spending decisions, just check your “In My Pocket” balance, and you know if you’re good to go or if you should hold back.

Another plus? Automatic tracking.

PocketGuard syncs with your bank accounts, categorizes your transactions, and even finds ways to cut down on recurring bills.

If you’re subscribed to five streaming services (been there), it’ll flag that and help you reduce unnecessary expenses.

Now, let’s talk about the free vs. premium versions.

The free plan covers basic budgeting and spending tracking, but if you want goal setting, custom spending categories, and advanced reporting, you’ll need PocketGuard Plus.

If you just need a simple way to avoid overspending, the free version might be enough.

So all in all, if impulse spending is your biggest ADHD money struggle, PocketGuard is 100% worth checking out.

Also read: Best ADHD productivity apps for iPhone

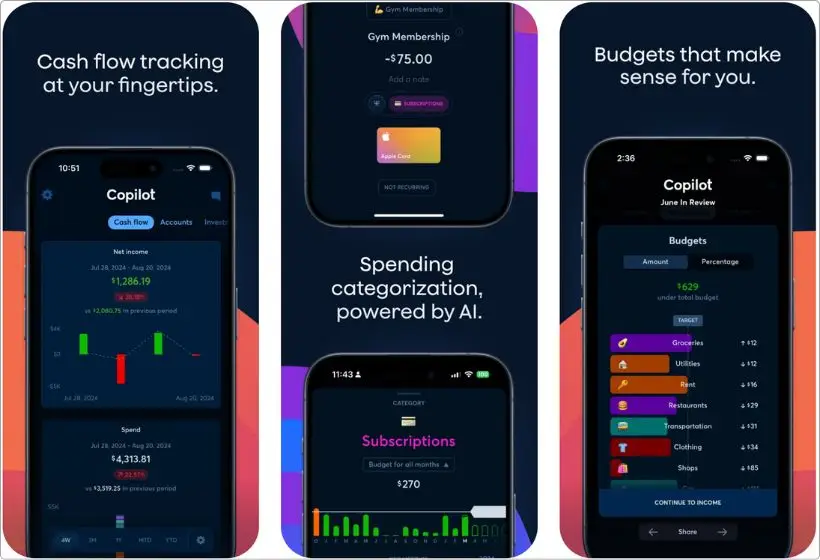

6. Copilot – Best for Customizable Budgeting

Pros:

- Highly customizable.

- AI-powered insights.

- Beautiful, distraction-free interface.

- Supports investment tracking.

Cons:

- No free version.

- No shared budgeting.

- Can take some time to set up properly.

Price: $13/month or $95/year.

Get it from: App Store

You know how some budgeting apps force you into rigid categories that don’t fit your life?

Yeah, that drives me nuts.

ADHD brains need flexibility, and that’s exactly what Copilot delivers.

Right out of the gate, Copilot feels different.

The app is designed to work around you, not the other way around.

You can customize your spending categories, tweak your budget in real time, and even rename transactions so everything makes sense to you.

If other ADHD budgeting apps feel like trying to fit into someone else’s system, Copilot is like designing your own.

Another standout feature?

AI-powered spending insights.

Copilot automatically categorizes transactions and learns from your habits, so over time, it gets smarter at tracking where your money goes.

For ADHD users who forget to check their budget (or just don’t have the energy), this kind of automation is a lifesaver.

Visually, Copilot is stunning.

It’s one of the cleanest, most ADHD-friendly interfaces I’ve seen—no clutter, no overwhelming spreadsheets, just a sleek, intuitive dashboard that makes managing money feel less stressful.

It also syncs effortlessly with Apple devices, which is a huge plus if you’re deep in the iOS ecosystem.

But Copilot isn’t free.

At $13/month or $95/year, it’s on the pricier side, but you do get a free trial to test it out.

Also, there’s no shared budgeting, so if you manage finances with a partner, this isn’t the best pick.

Bottom line?

If you need a budgeting app that adapts to YOU instead of the other way around, Copilot is worth every penny.

The customization, automation, and clean design make it one of the best ADHD-friendly budgeting tools out there.

7. Quicken Simplifi – Best for Simplified Budgeting

Pros:

- Super easy to use.

- Customizable spending watchlists.

- Automatically syncs with your bank and categorizes transactions.

- Great for tracking daily expenses and long-term financial goals.

Cons:

- No free version.

- Bank syncing can sometimes take a day to update.

Price: $5.99/month.

Get it from: App Store

Look, not everyone needs (or wants) a complex budgeting system.

Some people just want a straightforward, no-BS money tracker that helps them stay on top of spending without a million settings to tweak.

That’s exactly what Quicken Simplifi is.

From the moment you open the app, it feels clean, simple, and stress-free.

Unlike some budgeting apps that bombard you with charts and graphs, Simplifi keeps things focused.

You see what you have, what you’ve spent, and what’s left in your budget.

That’s it.

One feature I LOVE? Spending watchlists.

If you struggle with impulse spending (Amazon hauls, takeout, random gadgets—been there), you can set up a watchlist for specific spending categories.

The app will warn you if you’re getting close to your limit, helping you rein in bad habits without obsessively checking your budget.

Another ADHD-friendly feature is automatic transaction tracking.

You sync your bank, and the app automatically categorizes your expenses.

It’s not as detailed as YNAB or Monarch, but if you just want a simple way to see where your money is going, it does the job beautifully.

And yes, investment tracking is included.

If you have stocks, a 401(k), or other investments, you can view your portfolio alongside your budget without needing a separate app.

This makes Simplifi a great one-stop financial hub for ADHD users who don’t want to juggle multiple platforms.

Now, the downsides: Simplifi isn’t free, but at $5.99/month, it’s cheaper than YNAB, Monarch, and Copilot.

Also, while it has investment tracking, it doesn’t go as in-depth as a dedicated investment app like Personal Capital.

But if you ask me, just give it a shot. It’s simple, clear, and designed with ADHD in mind—definitely worth trying.

My Final Take

After testing and researching these apps, here’s my personal recommendation:

- If you want the best all-around ADHD budgeting tool, go with YNAB.

- Snoop is the best balance of smart automation and budgeting insights.

- Need a cash-based ADHD-friendly approach? Weekly is hands-down the best option.

- If you want a powerful, all-in-one financial management app, Monarch Money is the way to go.

- If overspending is your biggest issue, PocketGuard will help you rein it in.

- Copilot lets you tweak everything to fit your unique budgeting style.

- And if you just want a simple, no-BS money tracker, Quicken Simplifi does the job beautifully.

At the end of the day, the best ADHD budgeting app is the one you’ll actually use.

So find the one that clicks with your ADHD brain and start taking control of your finances.

FAQs

What’s the best free budgeting app for ADHD?

If you’re looking for a free option, Snoop is the best pick because it offers smart spending insights, automatic tracking, and AI-powered suggestions—all without costing a dime. Apple’s built-in Wallet & Budgeting tools (especially if you use Apple Card) can also be a decent free alternative.

Is YNAB really worth the price for ADHD users?

Absolutely. If you’re willing to commit to it. YNAB isn’t just an app; it’s a complete money management system that teaches you how to give every dollar a job, avoid impulsive spending, and build better financial habits. If you struggle with traditional budgets, YNAB can be life-changing.

What’s the easiest budgeting app for ADHD?

If you get overwhelmed easily and just want something super simple, Quicken Simplifi is a fantastic choice. It automatically tracks spending, provides a clear overview of your finances, and doesn’t require much setup or maintenance.

Which budgeting app helps the most with impulse spending?

PocketGuard is designed specifically to help ADHD users control overspending. It shows you exactly how much money is safe to spend after factoring in bills and savings goals, so you don’t accidentally drain your bank account on impulse buys.

What’s the best ADHD budgeting app for couples?

Monarch Money is the best app for shared budgeting, as it allows multiple users to manage finances together. If you and your partner/spouse want to track expenses, savings goals, and investments in one place, Monarch is a solid choice.

Are ADHD-friendly budgeting apps really different from regular budgeting apps?

Yes. ADHD-friendly apps tend to have simpler interfaces, more automation, and better visual organization to prevent overwhelm. Apps like YNAB, Weekly, and PocketGuard focus on breaking tasks into bite-sized, ADHD-friendly steps, making budgeting feel less stressful and more manageable.

What’s the best ADHD budgeting app for cash-based spending?

If you prefer cash-based budgeting (or struggle with digital tracking), Weekly is perfect. It helps you allocate your money in weekly chunks, mimicking a physical cash envelope system without the hassle of actual envelopes.

Can budgeting apps help me get out of debt?

Yes. YNAB and Monarch Money are particularly great for debt payoff strategies because they help you create a realistic plan for tackling debt while staying on top of other expenses. PocketGuard can also be useful for keeping spending in check so you can put more money toward debt repayment.