10 Must-Have Money Apps for College Students (2025)

If you’re here, you’re probably a college student trying to get your money in order without losing your mind. Good. You’re in the right place.

College is expensive, budgeting is confusing, and it’s easy to let it all slide until you’re broke again. I’m not here to judge you for that. I’m here to help you fix it.

Below, I’m sharing the best finance apps that actually work for students.

Apps that help you track your spending, avoid overdraft fees, cancel those sneaky subscriptions, save a bit more, or even start investing with literal spare change.

I want this list to be useful, not bloated with junk or “sponsored” nonsense I wouldn’t recommend myself. Just real options you can pick from today to make your money feel a little less stressful.

Scroll through, find what fits you best, and start taking control of your budget while everyone else is still winging it.

Table of Contents

- 1. PocketGuard – Best for Simple Overspend Alerts

- 2. Monarch Money – Best for Mint-Like Tracking at a Low Cost

- 3. YNAB – Best for Zero‑Based Budgeting Discipline

- 4. Goodbudget – Best for Envelope‑Style Budgeting

- 5. Chime – Best No‑Fee Student Banking

- 6. Capital One MONEY – Best Student-Friendly Checking with Savings Tools

- 7. Discover Cashback Debit – Best for Earning Rewards on Spending

- 8. Acorns – Best for Micro‑Investing Spare Change

- 9. Fidelity Youth Account – Best for Real Investing Learning Tools

- 10. Self – Best for Building Credit from Scratch

- My Final Take

- FAQs

1. PocketGuard – Best for Simple Overspend Alerts

Pros:

- Shows how much you can actually spend

- Auto-tracks expenses from all accounts

- Helps prevent overdrafting

Cons:

- Limited free version

- Can be too simple for advanced budgets

If you’re someone who just wants to know “Can I afford this?” without doing a million calculations, PocketGuard is your new best friend.

This app is designed for people who don’t want to stare at spreadsheets or set 37 budgeting categories they’ll forget in a week.

You connect your bank accounts, credit cards, maybe even your student loan servicer, and it automatically tracks everything.

But the magic is in the “In My Pocket” number.

That’s how much you can safely spend right now without wrecking your budget or overdrafting your account. So if you’re about to hit checkout on some late-night online shopping, you can see at a glance if that’s actually a good idea.

It’s not going to lecture you. It just lays it out in black and white.

And for college students who are busy, stressed, and tired of worrying if buying coffee will lead to a $35 overdraft fee, this is clutch.

The free version covers the basics, and for a lot of students, that’s enough.

If you want to get fancy with custom categories or see detailed spending trends, there’s a paid version too. But honestly… Start with free. See if it helps you feel more in control before you pay for anything.

PocketGuard isn’t going to make you rich overnight.

It won’t invest your spare change or cancel your subscriptions. But if you want one simple app to keep you from spending more than you have, it’s hard to beat.

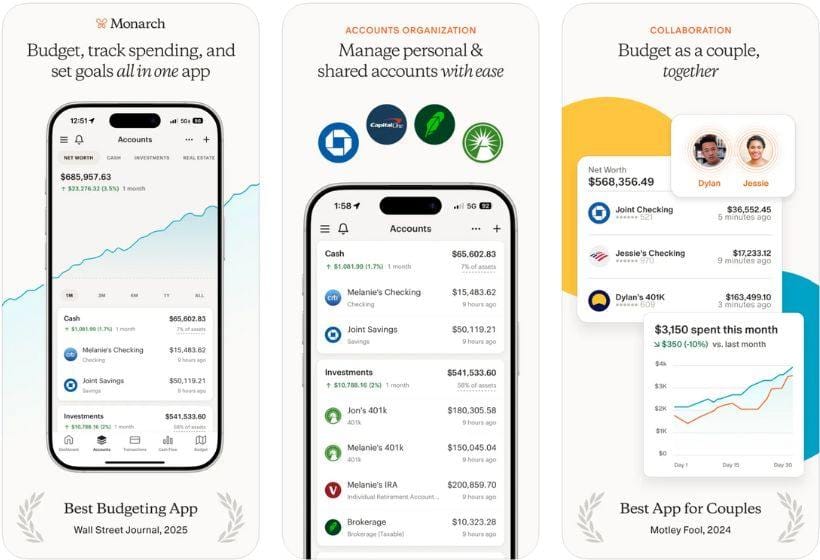

2. Monarch Money – Best for Mint-Like Tracking at a Low Cost

Pros:

- Tracks all accounts in one place

- Great for long-term planning

- User-friendly, clean interface

Cons:

- Paid after free trial

- Can be overkill for super simple budgets

If you’re the type who misses Mint or just wants that all-in-one dashboard vibe without selling your soul to ads and data tracking, Monarch Money is honestly one of the best replacements around.

Think of it as your personal finance command center.

You link all your accounts—checking, savings, credit cards, loans—and it gives you a clear view of everything in one place. No more logging into five apps to see where your money went.

It automatically categorizes transactions, so you can see exactly where that “fun money” is really going.

What sets Monarch apart is it’s designed to help you actually plan ahead.

Want to save for spring break? Need to budget rent, groceries, and car payments without screaming? Monarch lets you build real, customizable budgets and even do long-term goal tracking so you can see if you’re on track or totally screwed (in a kind, helpful way).

And unlike Mint, Monarch doesn’t bombard you with credit card ads or sell your data. It’s built by people who literally used to work on Mint, who saw the writing on the wall and decided to do it better.

It’s not totally free—there’s a free trial, then it costs a few bucks a month.

But if you’re serious about wanting to know exactly where your money’s going, it’s worth it. College is the best time to build these habits, so you’re not wondering why your credit card bill is a horror story.

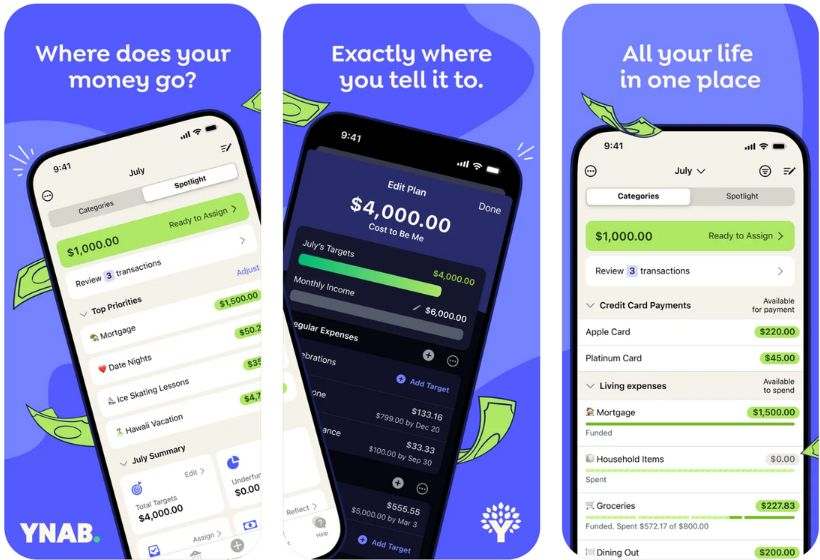

3. YNAB – Best for Zero‑Based Budgeting Discipline

Pros:

- Makes you give every dollar a job

- Great for avoiding surprises

- Helps you really see where money goes

Cons:

- Costs money after trial

- Takes a bit to get used to

Okay, so let’s be real: YNAB isn’t for people who want to “kind of” budget. This is the app you get if you’re serious about actually knowing where every dollar is going.

It’s called “You Need A Budget” for a reason. It doesn’t sugarcoat it.

You put in every dollar you have, and you tell it where it’s going to go. Rent. Food. Books. Whatever. Nothing’s just floating around waiting to “disappear.”

And yeah, it can feel weird at first. It’s not automatic like some other apps.

You have to sit down and actually do it. But that’s kind of the whole point. You can’t half-ass this. It’s for people who are tired of seeing $0 in their account and wondering how it happened.

The best part… It forces you to plan ahead. If you know next month’s rent is coming, you start saving now. No more “oh crap” moments when your landlord’s knocking.

It’s not free forever—you get a trial, then it’s a subscription.

But honestly… If you use it right, you’ll save way more than it costs. And if you’re willing to put in a little effort, it’ll change how you think about money for good.

Look, if you want easy and lazy, pick something else. If you want to actually fix your money habits before they turn into adult-sized problems, give YNAB a real shot.

4. Goodbudget – Best for Envelope‑Style Budgeting

Pros:

- Super simple concept

- Helps you plan spending ahead

- Great for people who like old-school methods

Cons:

- Manual tracking (no bank syncing)

- Not ideal for people who want “set it and forget it”

Alright, let’s talk about Goodbudget.

This one’s for you if you’re the kind of person who wants to really know where your money is going, but you don’t want anything complicated.

It’s basically the old-school envelope system your grandma might have used.

You decide what each category gets—rent, groceries, eating out, whatever—and you “fill” those envelopes digitally. Once it’s empty, you’re done spending in that category. No cheating.

Honestly… It’s kinda refreshing.

It forces you to make choices before you even swipe your card. That late-night takeout hits different when you see your “food” envelope is empty.

But here’s the thing—you have to do it yourself.

It doesn’t automatically pull in your transactions from your bank. You enter stuff manually. Some people hate that. But I think that’s the whole value—it makes you pay attention.

It’s free for basic use, which is perfect if you’re in college and don’t want another subscription in your life.

And there’s a paid tier if you want to budget across multiple devices or for fancier features—but honestly, start free.

If you want a budgeting app that doesn’t sugarcoat anything, makes you really plan, and keeps you honest about what you can spend, Goodbudget is one of the simplest, most no-BS ways to do it.

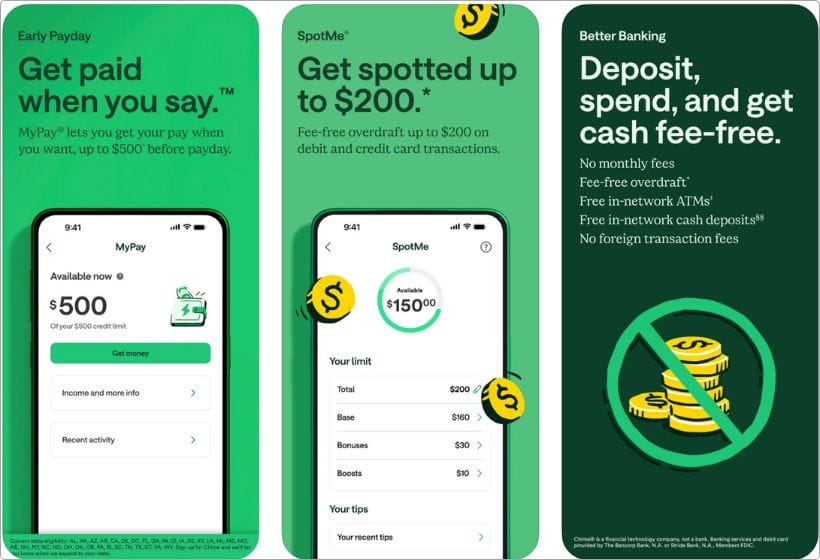

5. Chime – Best No‑Fee Student Banking

Pros:

- No monthly fees or minimum balance

- Early direct deposit (get paid faster)

- Great mobile app

Cons:

- No physical branches

- Can’t deposit cash easily

You know, traditional banks love hitting you with fees.

Overdraft fees. Maintenance fees. Minimum balance fees. It’s ridiculous when you’re in college and barely have enough for lunch.

That’s why Chime is so good for students.

It’s built to be no fee, plain and simple. You won’t get charged for having $4 in your account. There’s no “oh you didn’t keep $1000 in here? That’ll be $12 a month.”

Plus, if you have a job and set up direct deposit, Chime lets you get paid up to two days early. Not a gimmick, it actually works. When you’re living paycheck to paycheck, that can be the difference between covering rent on time or not.

The mobile app is super clean and easy to use.

You can check your balance in seconds, get transaction alerts, and even block your card if you lose it after a party (we’ve all been there).

But it’s not perfect. If you love going to a branch and talking to a human, this isn’t for you. And depositing cash can be a hassle—you have to do it at certain partner locations.

But for most students… You want an account that’s free, easy to manage on your phone, and doesn’t punish you for being broke sometimes.

That’s Chime in a nutshell.

If you’re tired of traditional banks nickel-and-diming you to death, this is an easy switch.

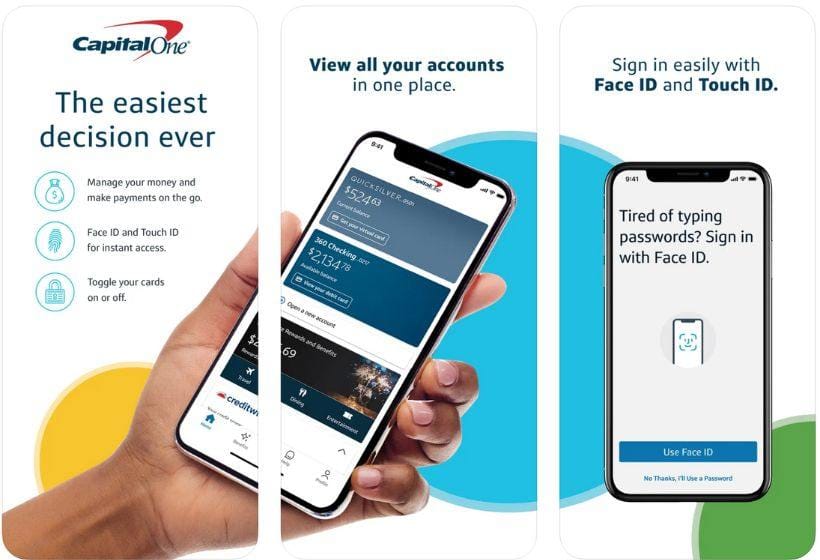

6. Capital One MONEY – Best Student-Friendly Checking with Savings Tools

Pros:

- No monthly fees or minimums

- Built-in savings goals

- Easy parental monitoring (if needed)

Cons:

- No overdraft (can be annoying if you’re used to it)

- Online-first experience

Alright, let’s talk about Capital One MONEY.

This is honestly one of the best checking accounts designed for students, even younger ones, but honestly, it’s great through college, too.

And there are no monthly fees. None. No “minimum balance” requirements either. You don’t have to keep $500 sitting there doing nothing just to avoid fees. That alone makes it solid for students who don’t have much extra cash.

It also has some smart built-in features that actually help you save.

You can set up goals right in the app. Think spring break trip, new laptop, emergency ramen fund—whatever. It lets you mentally separate that cash so you don’t blow it all at Taco Bell.

Another thing… If you’re on the younger side or your parents want to help keep an eye on things, there’s a built-in way for them to monitor the account. Some people think that’s lame, others love it because it makes it easier to get help with budgeting.

Now, one downside… There’s no overdraft protection that lets you spend money you don’t have.

For some people, that’s annoying. But honestly… It’s kind of the point. You can’t overdraft and get slapped with a $35 fee. It just declines. Harsh but fair.

Also, it’s an online-first experience.

Don’t expect to walk into a branch for everything. But the app is easy to use, you can lock your card if you lose it, and you’ll always know what’s in your account.

If you want simple, no-fee banking with solid savings tools built in, Capital One MONEY is a really solid pick for college life.

7. Discover Cashback Debit – Best for Earning Rewards on Spending

Pros:

- 1% cashback on debit card purchases

- No monthly fees or minimums

- Great mobile app experience

Cons:

- Cashback has a monthly cap

- Fewer physical branches

You know, most student checking accounts don’t give you anything for using them. They’re like, “Congrats on not overdrafting—here’s nothing in return.”

Discover is different. You actually get 1% cashback on your debit card purchases.

Yeah, like a credit card—but without worrying about getting into debt. It’s capped at a certain amount each month, but still. Free money for stuff you were gonna buy anyway.

There are no monthly fees. No minimum balances. You don’t have to stress about keeping hundreds just to avoid getting dinged with charges you can’t afford.

It’s student-friendly without pretending it’s doing you a favor for the “privilege” of being their customer.

The app is really solid, too. You can freeze your card in two seconds if you lose it (or think you did after a night out). You can see transactions instantly, deposit checks with your phone camera, all the usual modern stuff you’d expect.

Downsides? The cashback caps out monthly, so you’re not getting rich here—it’s just a nice perk. And if you want to go sit down with a teller at a branch? Yeah, good luck. Discover’s online-first, so you’re not getting that.

But honestly… If you’re a student who wants to actually get something back from your checking account, this is one of the best deals out there. No fees. Simple app. Free money back in your pocket. Hard to argue with that.

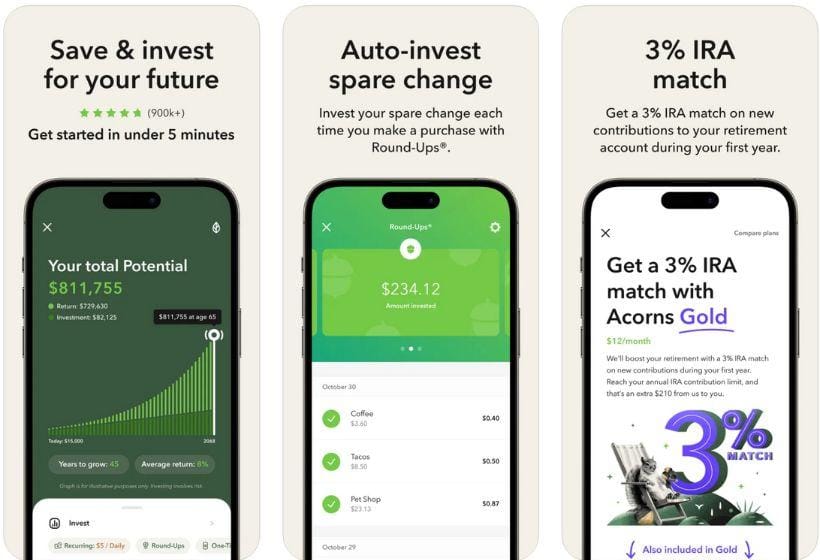

8. Acorns – Best for Micro‑Investing Spare Change

Pros:

- Invests your spare change automatically

- Super easy to set up

- Great for beginners

Cons:

- Monthly fee (even if small)

- Limited control over investments

I know most college students aren’t thinking about investing.

You’re busy just trying to pay rent and maybe have a little fun money left over. But the thing is, starting small now can make a huge difference later.

That’s where Acorns comes in.

It’s honestly one of the easiest ways to get into investing without overthinking it. You just connect your debit or credit card, and every time you buy something, Acorns rounds it up to the next dollar and invests the change.

Buy a coffee for $3.50? Acorns grabs 50 cents and puts it to work in a diversified portfolio. It’s automatic. You don’t have to remember to do anything.

I love that it’s so low-pressure. You don’t need to know the stock market. You don’t have to pick individual companies or worry about timing anything. It just quietly builds up over time while you’re living your life.

But I won’t lie: there’s a small monthly fee.

It’s pretty cheap, but if you’re only investing a few bucks a month, it can feel like it eats into your gains. That’s something to think about.

Also, you don’t get to micromanage what you’re investing in—it’s pre-built portfolios designed for ease.

Still, for most students… Acorns is a super chill way to start investing now, even if all you can afford is spare change. It helps you build the habit, and that’s honestly the most important part.

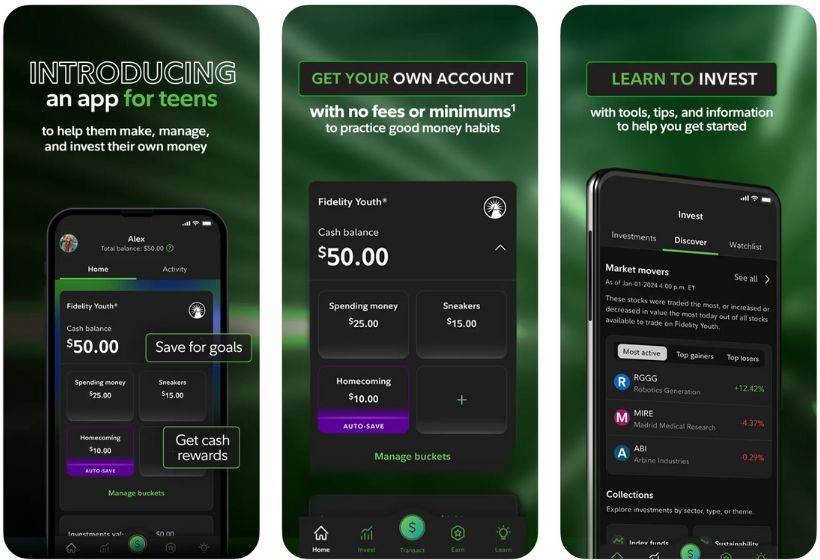

9. Fidelity Youth Account – Best for Real Investing Learning Tools

Pros:

- Real brokerage account for teens & students

- No account fees or minimums

- Teaches you real investing early

Cons:

- You have to be 13–17 to open (but stay open after)

- Requires parent/guardian to set up initially

Alright, let’s talk about getting into real investing while you’re still in college (or even high school). This isn’t rounding up your coffee change—it’s buying actual stocks and ETFs, seeing the ups and downs, and learning for real.

Fidelity Youth Account is one of the best ways to do that without getting hit by fees or crazy barriers.

It’s designed for teens and students. You’ll need a parent or guardian to help you open it if you’re under 18, but once it’s set up, you’re in control.

This isn’t a toy. It’s a real brokerage account.

You can buy and sell real stocks and ETFs, just like the grown-ups do. And there’s no account minimum or monthly fee. That’s huge if you’re in college and don’t have a ton of money lying around.

Honestly… I wish stuff like this existed when I was younger. Instead of being terrified of investing or thinking it was just for rich people, you get to actually try it with small amounts.

You learn by doing. That’s the best way to avoid dumb mistakes when you’re older and the stakes are bigger.

Now, heads up: you’ll need that initial parent setup if you’re 13–17.

And even if you’re 18+, you might want to check it out because once you’re in, you’re good. It’s not some kid-only thing forever—it just helps you start early.

If you want to actually learn how investing works now, while your friends are still avoiding their bank balance, this is one of the best places to start.

10. Self – Best for Building Credit from Scratch

Pros:

- Helps you build credit with no credit card

- Reports to all three major credit bureaus

- Flexible payment plans

Cons:

- Costs money to use

- You don’t get immediate access to the loan funds

Let’s have a real talk about credit. Most people don’t think about it in college.

Then one day they need to rent an apartment, get a car loan, or even just sign up for a phone plan, and suddenly—bam. They have no credit score, or it’s trash.

That’s where Self comes in.

It’s honestly one of the easiest ways for students to start building credit safely. No need for a traditional credit card you’re afraid of maxing out.

Here’s how it works: you sign up for a “credit builder loan,” which is basically a forced savings plan. You pay a small amount each month—like $25 or so—and they report those payments to all three major credit bureaus. At the end of the term, you get your money back (minus some fees).

So you’re building credit history and a savings habit at the same time.

Yeah, it costs a bit. You won’t get all your payments back because there are fees. And you don’t get the money right away—it’s locked in savings until you finish. That’s not ideal if you’re broke and need cash now.

But if you’re thinking long-term… It’s a solid move.

A lot of students graduate with $0 credit history and get screwed over with high interest rates or flat-out rejections. Self helps you avoid that future headache, one little payment at a time.

If you want to do yourself a favor and start building credit now—without a credit card you’re worried about misusing—this is honestly one of the best ways to do it.

My Final Take

Look, I know money is probably the last thing you want to think about in college.

You’ve got classes, friends, work shifts, late-night pizza runs—it’s a lot. But figuring this stuff out now is one of the best gifts you can give yourself.

You don’t need to download all these apps today. Seriously. That’s overwhelming and pointless.

Pick one or two that actually fit you. The one that stops you from overdrafting. The one that helps you save for that trip. The one that quietly invests your spare change while you’re busy being 20-something.

That’s all it takes to start.

Because here’s the truth: no one’s going to do this for you. Your bank sure won’t. And “future you” will be so damn grateful you gave even half a crap about this now.

So yeah—scroll back up, pick one, and give it a try. That’s it.

And if you’ve got other apps you swear by, or questions about any of these, drop them in the comments. Let’s help each other out. College is hard enough. Your money doesn’t have to be.

FAQs

What is the best budgeting app for college students?

Honestly… It depends on what you want. If you want something super simple and automatic, PocketGuard is solid. If you’re ready to get serious and give every dollar a job, YNAB is the one people swear by. Both help you avoid that classic “where did my money go?” feeling.

Are finance apps safe for students to use?

Yeah, most major finance apps use bank-level encryption and security. But you still want to be smart: pick well-known apps with good reviews, use strong passwords, and enable two-factor authentication when you can. No app can make you invincible, but they’re generally safe if you use common sense.

Do I need to pay for a budgeting app?

Not always. Apps like Goodbudget or PocketGuard have free versions that work well for most students. YNAB and Monarch Money cost a little after their free trials, but a lot of people find it’s worth it if it helps them actually stick to a budget.

Can I invest money as a college student?

Absolutely—and you don’t need to be rich to start. Apps like Acorns help you invest your spare change automatically, and Fidelity Youth gives you real investing experience without account fees. Even tiny amounts add up over time. Starting now is honestly one of the smartest moves you can make.

What’s the best bank account for college students?

It depends on what you want most. Chime is great if you want no fees and early paychecks. Capital One MONEY is solid for no minimums and easy savings goals. Discover Cashback Debit even gives you 1% back on spending, which is rare for a debit card.

How do I build credit in college without a credit card?

Self is perfect for that. Instead of a credit card, it’s a “credit builder loan” that reports your payments to the credit bureaus. You pay a bit each month, it builds your credit history, and you get the money back (minus fees) at the end. Way safer than running up card debt.

Should I use more than one finance app?

You can, but don’t overwhelm yourself. Start with one that solves your biggest problem—budgeting, saving, investing, credit building. Once you’re comfortable, you can add another if it helps. It’s better to actually use one app well than download five and ignore them all.