TOP 7 iPhone Apps for Building Credit (2025)

Look, building credit isn’t fun.

It’s not flashy.

But it’s one of those things you’ve gotta do if you ever wanna get approved for stuff like a car loan, apartment, or even a good credit card.

And yeah, most advice out there sounds like it was written by a bank.

Boring.

That’s why I put together this list of iPhone apps that actually help you build credit, without all the confusing talk.

These apps? They’re simple.

They work.

And you don’t need to be some finance nerd to use them.

Let’s dive into the best iPhone apps for building credit in 2025, starting with the one I recommend to almost everyone.

Table of Contents

- 1. Self – Best Overall Credit Builder App

- 2. Experian Boost – Best for Boosting Credit Fast

- 3. Credit Karma – Best for Free Credit Monitoring & Personalized Tips

- 4. Chime – Best for Building Credit with a Secured Card

- 5. Kikoff – Best $5 Credit Builder Plan

- 6. Grow Credit – Best Free Credit Builder for Subscriptions

- 7. Ava – Best for All-in-One Credit Building (Subscriptions + Savings)

- My Final Take

- FAQs

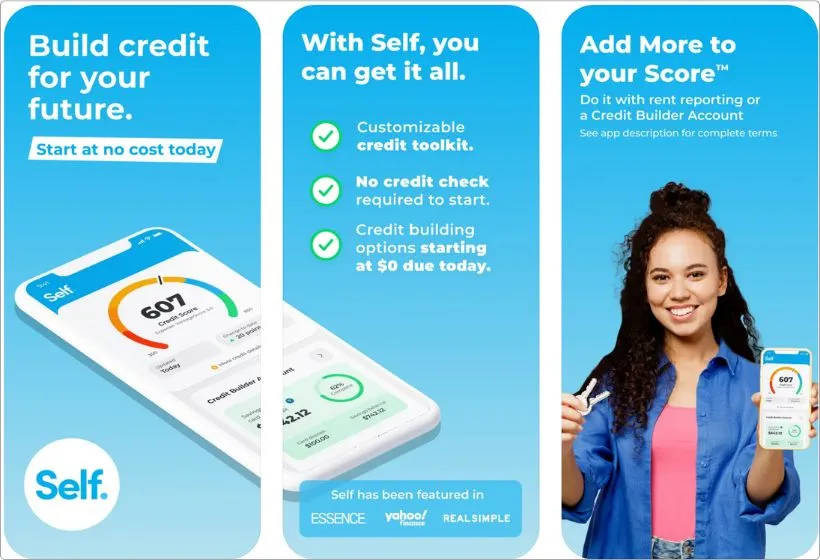

1. Self – Best Overall Credit Builder App

Pros:

- No credit check to get started

- Reports to all 3 credit bureaus

- Helps you save money while building credit

- Offers a secured credit card later

Cons:

- Has monthly fees

- Late payments can hurt your credit

Alright, so Self is one of those apps I always end up recommending — not because they pay me (they don’t), but because it actually works.

Here’s the deal: when you sign up for Self, you’re basically opening a Credit Builder Account. You pick a monthly plan (like $25 or $35), and instead of giving you that money upfront, Self holds it for you in a locked savings account (a CD, technically). You make your monthly payments, and every single one gets reported to Experian, Equifax, and TransUnion.

At the end of the term?

You get your money back, minus a small fee.

And by then, your credit history looks way better than it did before.

But wait, there’s more (I sound like an ad, I know) — after a few on-time payments and saving at least $100, you can unlock their Self Visa® Credit Card.

It’s a secured card, so you’re using your own money, but they report those payments too.

That’s double credit building.

It’s not instant magic, but if you’re serious about getting your score up, especially if you’re starting from scratch or rebuilding, Self is a no-brainer.

Since you’re serious about fixing your credit, tracking your spending should be next.

I’ve also rounded up the best budgeting apps for iPhone to help you stay on top of it all.

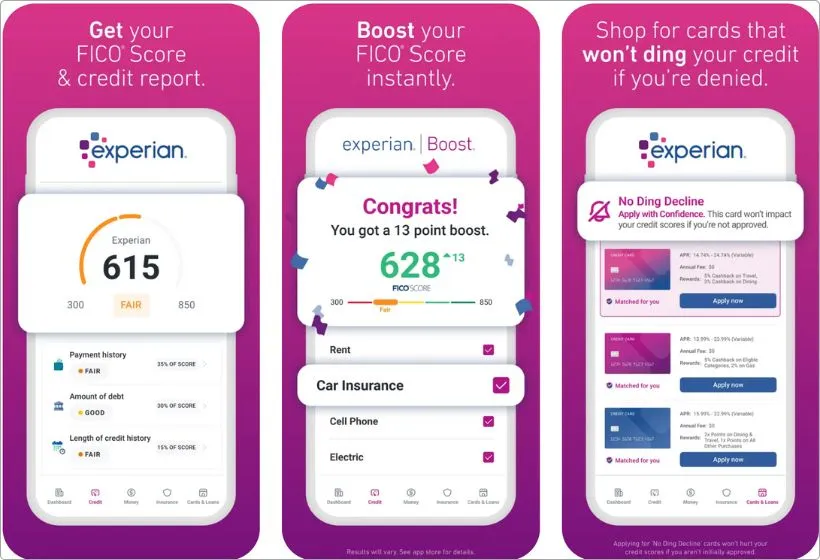

2. Experian Boost – Best for Boosting Credit Fast

Pros:

- Boosts your score instantly using bill payments

- Totally free to use

- No credit card or loan needed

- Tracks your Experian score in real time

Cons:

- Only affects your Experian credit file

- Doesn’t work if your name’s not on the utility bills

Alright, so Experian Boost is for the people who want to see a quick jump in their credit score without signing up for loans or credit cards.

It’s literally one of the easiest “hacks” out there — and it’s 100% legit.

So here’s how it works: you link your bank account, and Experian scans for recurring payments like Netflix, Spotify, phone bills, or even your electric and water bills. If you’ve been paying those on time (even if it’s just $15/month for Hulu), they’ll add that history to your Experian credit report.

It’s kinda wild when you think about it.

These are bills you already pay, but now they actually help your credit.

And because it updates instantly, you might see a little score boost right away, which is super helpful if you’re trying to qualify for a loan or a new card.

Now, small catch — Boost only affects your Experian score, not the other two (Equifax and TransUnion).

But honestly, lenders still use that data, and if it gives you a better rate or helps you get approved, it’s totally worth it.

So yeah, if you’re just getting started or need a quick win? Boost is a no-brainer.

Doesn’t cost you a penny and could literally improve your score today.

And if you’re forgetful with bills (no shame), use one of these bill reminder apps for iPhone to stay on track.

One late payment can mess up the whole boost.

3. Credit Karma – Best for Free Credit Monitoring & Personalized Tips

Pros:

- 100% free to use

- Shows your credit score and full reports

- Sends alerts for changes or new activity

- Recommends credit cards and loans based on your profile

Cons:

- Doesn’t show your Experian score

- Recommendations can feel a bit “salesy” sometimes

Credit Karma is one of those apps that almost everyone has heard of — and for good reason.

It’s like your credit sidekick, always chillin’ in your pocket, making sure you know exactly what’s going on with your credit.

Once you sign up (takes like 2 mins), you get access to your credit scores from TransUnion and Equifax.

You can check your report anytime, see what’s helping or hurting your score, and even get breakdowns of stuff like your credit usage, payment history, and total accounts.

But here’s the real MVP feature — it sends you real-time alerts.

Like if someone runs a credit check on you, or a new account pops up, you’ll get a notification ASAP.

That’s huge for catching errors or fraud early.

Plus, they’ve got this credit score simulator, where you can mess around with scenarios like “what if I paid off my card?” or “what if I opened a new loan?”

It’s not perfect, but it gives you a solid idea of what to expect.

Yeah, they recommend credit cards and loans; that’s how they make money.

But the cool part is they actually base those suggestions on your credit profile, not random ads.

So if you’re trying to build credit the smart way, Credit Karma can point you in the right direction.

All in all? It’s one of those “set it and forget it” apps — but with major upside.

4. Chime – Best for Building Credit with a Secured Card

Pros:

- No credit check to apply

- No annual fees or interest

- Reports to all 3 credit bureaus

- Works like a debit card but helps your credit

Cons:

- You need a Chime Checking Account to get started

- Not ideal if you want a traditional credit card with rewards

Alright, so here’s the deal with Chime — it’s not just a banking app anymore.

Their Credit Builder Visa® Card is straight-up fire for anyone trying to build credit from the ground up, without falling into credit card debt.

Here’s how it works: You move money into your Chime Credit Builder account, and that becomes your spending limit. No borrowed money, no interest charges. Just your own cash. Then, when you use the card, Chime reports those purchases and payments to all three credit bureaus, helping build your score every month.

The best part? There’s no credit check, no minimum deposit, and no sneaky fees.

So if your credit’s not great (or non-existent), they’re not judging.

You just need a Chime checking account and some steady income coming in.

And unlike traditional secured cards that lock up your deposit, with Chime, you can move money in and out easily.

You stay in control the whole time.

One thing though — it’s not gonna give you points or cash back or any of that.

This card is about one thing only: building your credit the clean way.

If you’re tired of being denied by big banks and just want a low-risk way to start growing your score, Chime is a solid move.

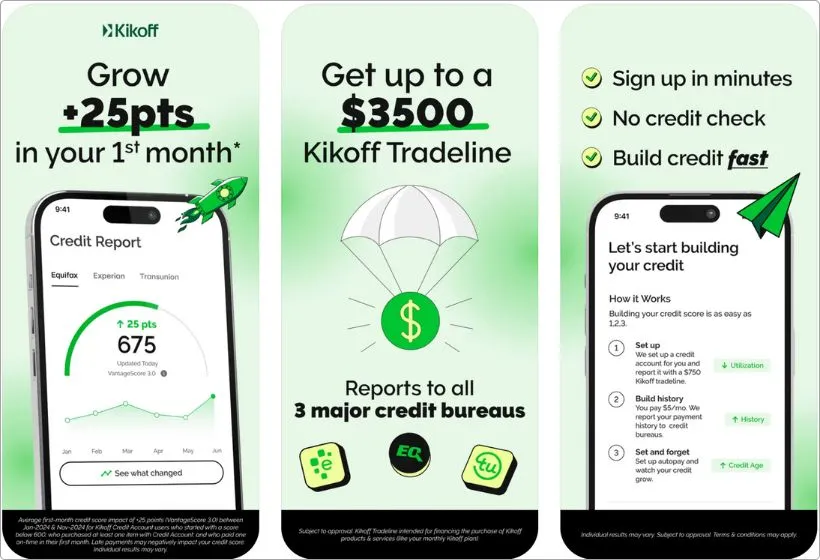

5. Kikoff – Best $5 Credit Builder Plan

Pros:

- Just $5/month — super affordable

- No credit check, no interest

- Reports to all 3 credit bureaus

- Easy approval, even with bad or no credit

Cons:

- Can’t use the credit line for outside purchases

- No physical card

Kikoff is one of those apps that makes you go, “Wait… that’s it?” — and yeah, that’s kinda the whole point.

It’s crazy simple, low-cost, and perfect for anyone who just wants to start building credit without getting tangled in credit card debt.

Here’s how it works: When you sign up, Kikoff gives you a $750 virtual credit line. But instead of swiping it at stores, you use it inside Kikoff’s own store to “buy” digital content — think finance courses, ebooks, etc. Doesn’t matter what you buy, though — what matters is that you’re making payments, and Kikoff reports those to Experian, Equifax, and TransUnion.

The kicker? You’re paying just $5 a month.

No interest. No extra fees.

Just $5 flat.

That’s cheaper than a coffee run, and it helps build your credit history every single month.

There’s no physical card, and you can’t use it like a normal credit line, but that’s not the point.

This is strictly for boosting your score, and for a lot of people, especially if your credit’s not looking too hot, it’s a perfect “foot in the door” kind of app.

So if you’re broke, rebuilding, or just don’t wanna risk messing up with a real card, Kikoff gives you a clean and easy path forward.

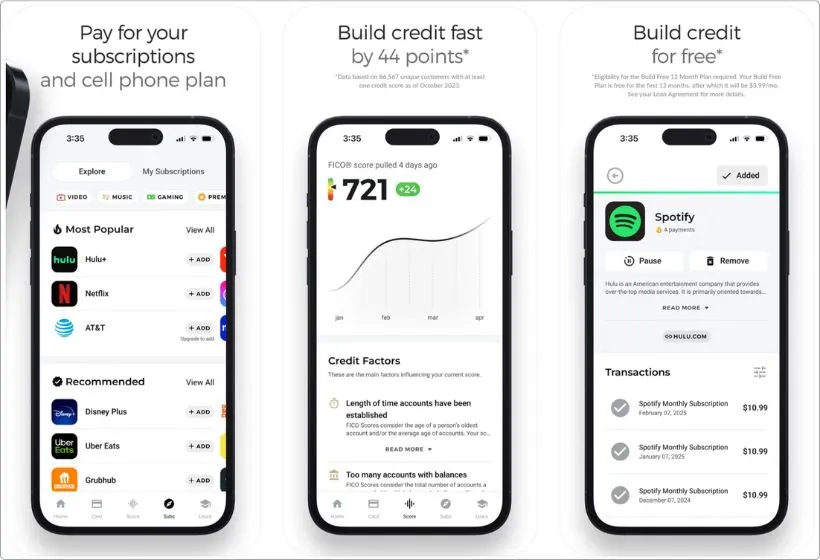

6. Grow Credit – Best Free Credit Builder for Subscriptions

Pros:

- Free plan available

- No credit check to apply

- Reports to all 3 credit bureaus

- Works with popular subscriptions like Netflix, Hulu, and Spotify

Cons:

- Can only use the card for subscription services

- Spending limit is pretty low

Grow Credit is a low-key one of the smartest ways to build credit, especially if you’re already paying for stuff like Netflix, HBO Max, or even your gym membership.

Here’s how it works: They give you a virtual Mastercard, and you link it to your favorite subscriptions. Then, every month when those services get billed, Grow covers the payment, and you pay them back. Those payments get reported to Experian, Equifax, and TransUnion, just like a regular credit card would.

Now here’s the sweet part — they offer a free plan, so if you just wanna dip your toes in, you can do it without spending a dime.

The free tier lets you cover one or two subscriptions (up to $17/month), but if you want more coverage, they’ve got premium plans starting at just $1/month.

There’s no credit check, no interest, and no late fees.

It’s all automated.

You just keep doing what you’re already doing (watching Netflix and chillin’), and your credit improves behind the scenes.

The only real downside?

You can’t use it for gas, groceries, or shopping.

It’s strictly for subscriptions.

But if you’re not ready for a real credit card yet, this is a chill, low-risk way to build credit every month.

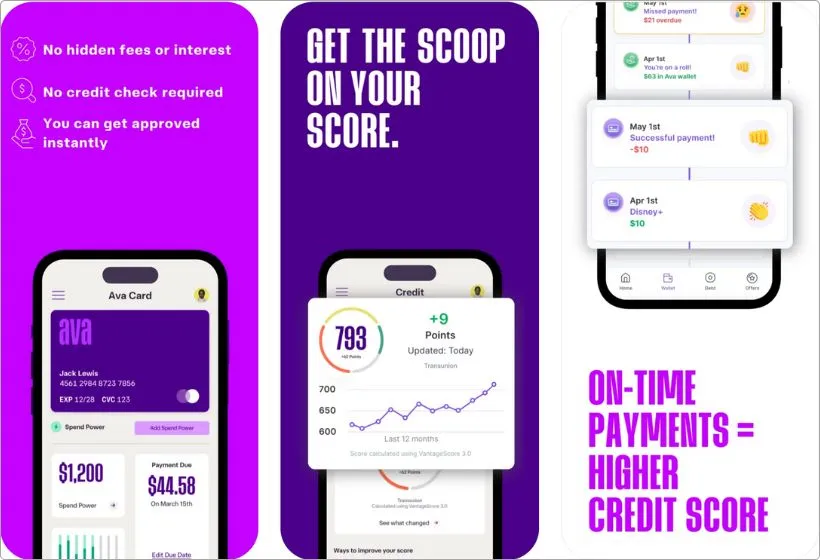

7. Ava – Best for All-in-One Credit Building (Subscriptions + Savings)

Pros:

- Builds credit with both subscriptions and savings

- Reports to all 3 credit bureaus

- No credit check to apply

- Fast reporting (as quick as 24 hours)

Cons:

- Monthly fee (starts at $6/month)

- Only works with approved subscriptions

Ava is like the grown-up version of Grow Credit.

It takes the same idea (build credit by paying for subscriptions), but levels it up with an optional savings feature that helps you hit more parts of your credit profile.

Here’s how it rolls: You get a virtual Ava Credit Builder Card, and you can use it to pay for over 60 approved subscription services — think Netflix, Verizon, Spotify, and more. Each time you pay through Ava, those on-time payments get reported to all three bureaus.

But here’s where Ava steps it up: they also offer a Save & Build plan, where you put as little as $25/month into a secure savings account.

Ava treats it like a mini loan and reports every contribution as an on-time loan payment.

That means you’re building credit history + credit mix in one go — a combo that can seriously move your score over time.

There’s no credit check, and setup takes just a few minutes.

It’s super beginner-friendly, but with that added savings feature, it’s also great for people who are tired of just watching the score and actually want to do something about it.

Downside? It’s not free — plans start at $6/month (or $9/month if you go monthly).

But if you want a smart, all-in-one setup to grow your score and your savings side-by-side, Ava hits the spot.

My Final Take

Alright, if you’ve made it this far, respect.

Seriously.

Most people want to build credit, but never actually take the steps.

So you’re already ahead.

Now, if you’re thinking, “just tell me what to pick,” here’s how I see it:

- Go with Self if you want the most well-rounded tool — it builds credit, helps you save, and even gives you a secured card.

- Try Experian Boost if you want a quick win using bills you already pay.

- Use Kikoff or Grow Credit if you’re broke but still wanna move the needle (they’re low-risk, super affordable).

- And if you’re ready to go all in? Ava gives you that subscription + savings combo that really builds a stronger credit profile over time.

Bottom line? You don’t need to be rich or even have good credit to start.

Just pick one, stick with it, and let the apps do their thing.

Credit doesn’t grow overnight, but with these tools in your pocket, you’re not just hoping — you’re actually building.

FAQs

Which app is best for beginners with zero credit history?

If you’re starting from scratch, Self, Chime, or Kikoff are solid picks. They don’t require a credit check, and they’re super beginner-friendly — just set it and forget it.

Can I use more than one credit-building app at the same time?

Yep, totally. A lot of people use Self + Credit Karma or Grow Credit + Experian Boost together. Just make sure you can manage your payments, because missing one will hurt more than help.

Does Self require a credit check to get started?

Nope! That’s one of the best things about Self — you can sign up without a hard credit check. It’s built for people who are either starting from scratch or trying to rebuild.

Does Experian Boost really increase my score instantly using bill payments?

Yup. If you’ve got utility bills, phone plans, or streaming services in your name and you’ve been paying on time, Boost can add them to your Experian credit file and bump your score within minutes.

Is Credit Karma truly free, and which credit scores does it show?

100% free — no catch. Credit Karma gives you your TransUnion and Equifax scores, not Experian. Still super helpful for tracking your credit and getting personalized tips.

Can Chime’s Credit Builder card be used like a traditional credit card?

Not exactly. You can’t carry a balance or spend money you don’t have. It works more like a debit card — you preload it, spend it, and Chime reports those payments like a credit card.

Does Kikoff provide a physical card, or can I use it for outside purchases?

Nah, Kikoff doesn’t give you a real card, and you can’t swipe it in stores. You can only use the credit line inside their app to buy digital content — the whole point is just to build credit with monthly payments.

What subscriptions can I pay with Grow Credit or Ava, and do they report to all bureaus?

Both support big names like Netflix, Hulu, Spotify, HBO Max, AT&T, Verizon, and more. And yes — Grow Credit and Ava both report to all three major credit bureaus, so your on-time payments help across the board.